Listen to the CEO Survey report and insights from our experts

Twelve months ago, we reported that nearly 40% of global CEOs believed their companies would no longer be viable in ten years’ time if they continued on their current path. The reinvention imperative this implied caught the attention of our clients, prompting thousands of conversations between PwC partners and CEOs around the world. ‘Are we in the 40% or the 60%?’ was a question many CEOs posed to themselves and their top teams during or following these discussions. Almost invariably, as they anticipated the magnitude of changes barrelling towards them, those leaders concluded that they needed to be more transformative in their approach if their organisation was to thrive in the decades ahead.

45%

of CEOs believe their company will not be viable in ten years if it stays on its current path.

This year’s Global CEO Survey, the 27th we’ve conducted, suggests that the vast majority of companies are already taking some steps towards reinvention. Yet even as CEOs attempt meaningful changes to their companies’ business models, they are even more concerned about their long-term viability. Although the 4,702 CEOs responding to this year’s survey were more optimistic about global economic growth than last year, 45% of them are still not confident that their companies would survive more than a decade on their current path. Among the other key findings:

- The impetus to reinvent is intensifying. CEOs expect more pressure over the next three years than they experienced over the previous five from technology, climate change and nearly every other megatrend affecting global business.

- Survival-conscious CEOs among the 45% who are less confident of their company’s viability are slightly more likely than other CEOs to have taken action aimed at reinventing their business models. Small company chief executives are more likely than their larger company counterparts to feel their company’s viability threatened.

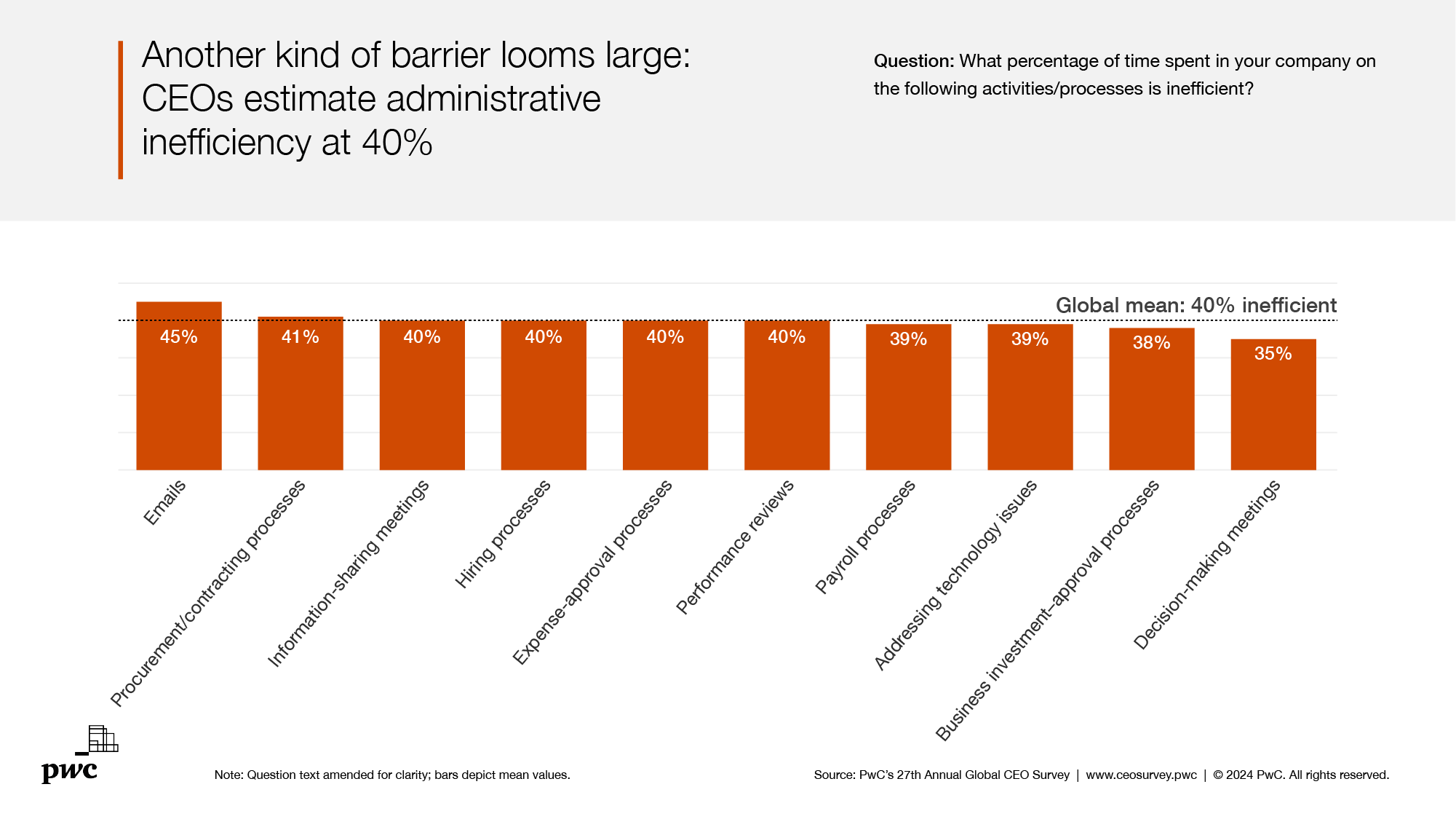

- CEOs perceive enormous inefficiencies across a range of their companies’ routine activities—everything from decision-making meetings to emails—viewing roughly 40% of the time spent on these tasks as inefficient. A conservative estimate of the cost of that inefficiency would be tantamount to a self-imposed US$10 trillion tax on productivity. Generative AI, which about 60% of CEOs expect to create efficiency benefits, could help relieve some routine burdens.

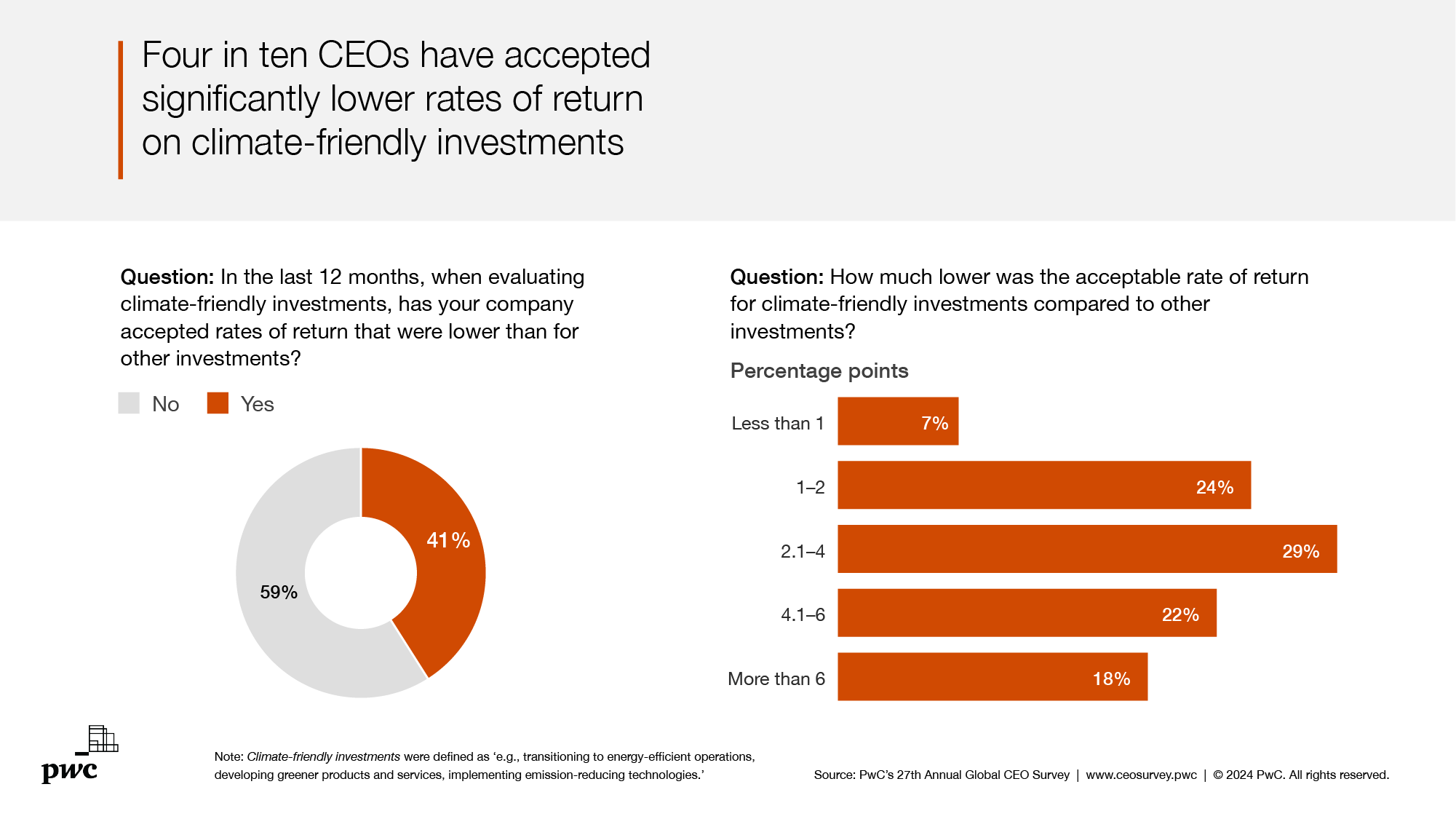

- Four in ten CEOs report that they have accepted lower hurdle rates for climate-friendly investments than for other investments—in the majority of cases, between one and four percentage points lower. This is clear evidence that some CEOs are willing to make complex trade-offs as they strive to boost the sustainability of their businesses.

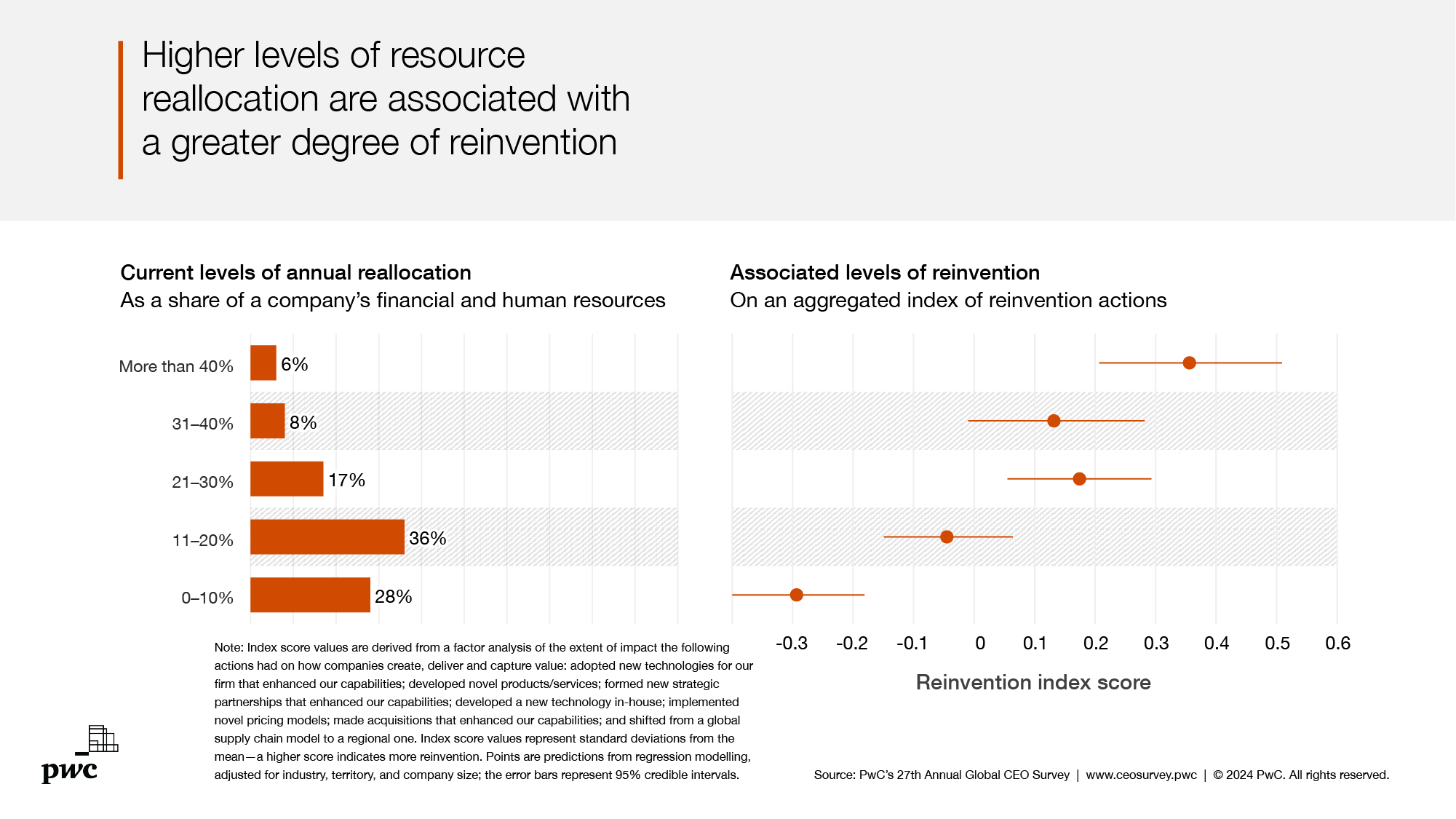

- Meanwhile, two-thirds of CEOs report reallocation of resources (financial and human) of 20% or less year to year. The connections among reallocation, reinvention and financial performance suggest that more aggressive reallocation—up to a point—is required to succeed.

The stakes are high, but so is CEO awareness of both the urgency to change and the need to deliver sustained outcomes for stakeholders and society. To clarify the nature of the challenge and the opportunities associated with meaningful business reimagination, we’ve organised this year’s report in nine sections under three themes.

The reinvention imperative

1. An enduring imperative to reinvent

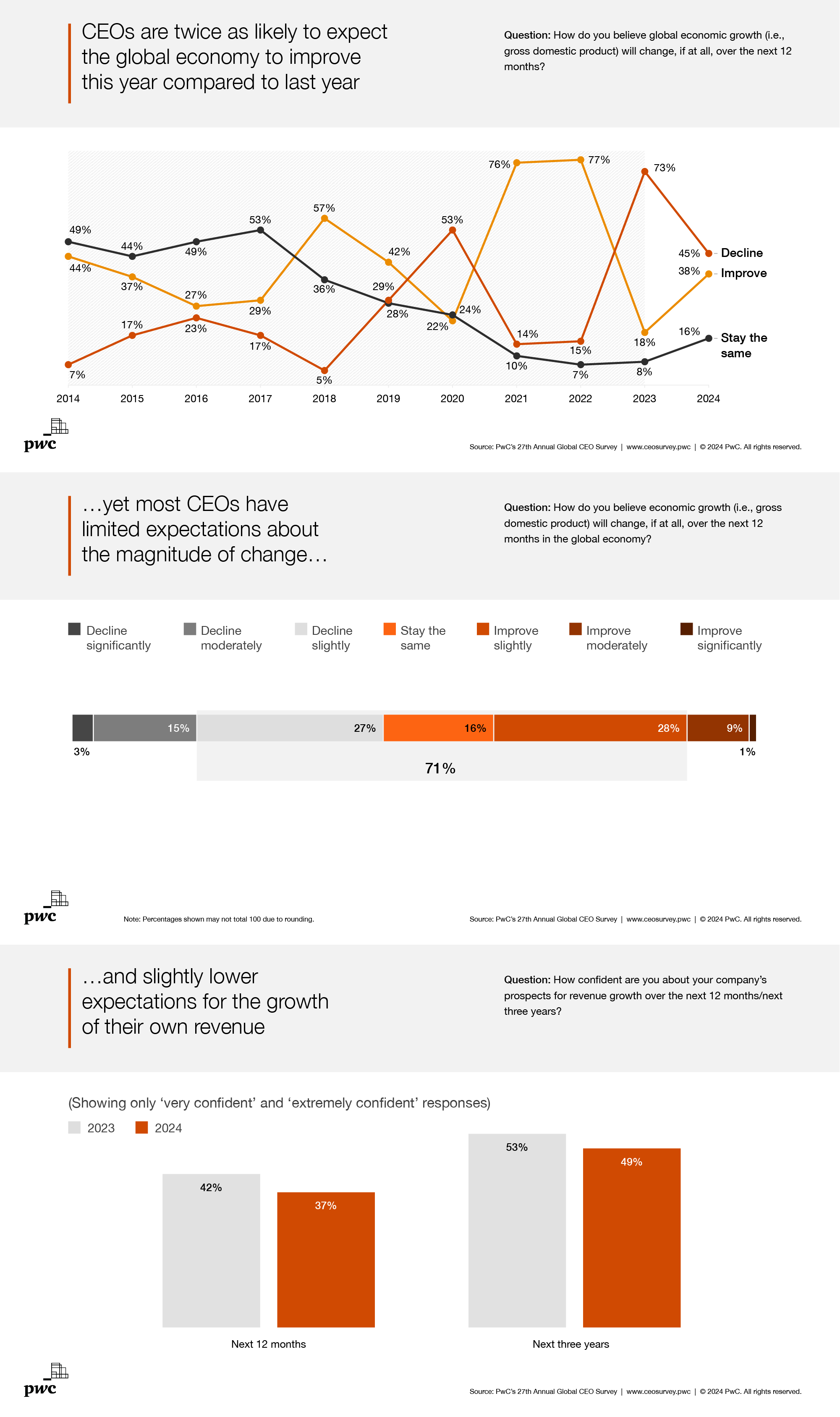

Technological disruption, climate change and other accelerating global megatrends continue to compel CEOs to adapt, as a whopping 97% of respondents to PwC’s 27th Annual Global CEO Survey report having taken some steps to change how they create, deliver and capture value over the past five years. During that span, 76% of CEOs took at least one action that had a large or very large impact on their company’s business model. That finding reflects a growing unease, as 45% of respondents doubted their company’s current trajectory would keep them viable beyond the next decade—up from 39% just 12 months earlier.

{kind=link}

The intensification of CEO worries about corporate viability does not appear to reflect near-term economic concerns. For example, CEOs are less likely than they were a year ago to anticipate a decline in global economic growth, and much more likely to expect growth will improve in 2024 (38% compared to 18% last year). Still, that doesn’t mean CEOs are unalloyed optimists: slightly more CEOs expect the global economy to contract in the coming year than expect it to improve. CEOs are also slightly less confident than last year in their own company’s prospects for revenue growth, over both the next 12 months and the next three years.

{kind=link}

2. Pressures and threats

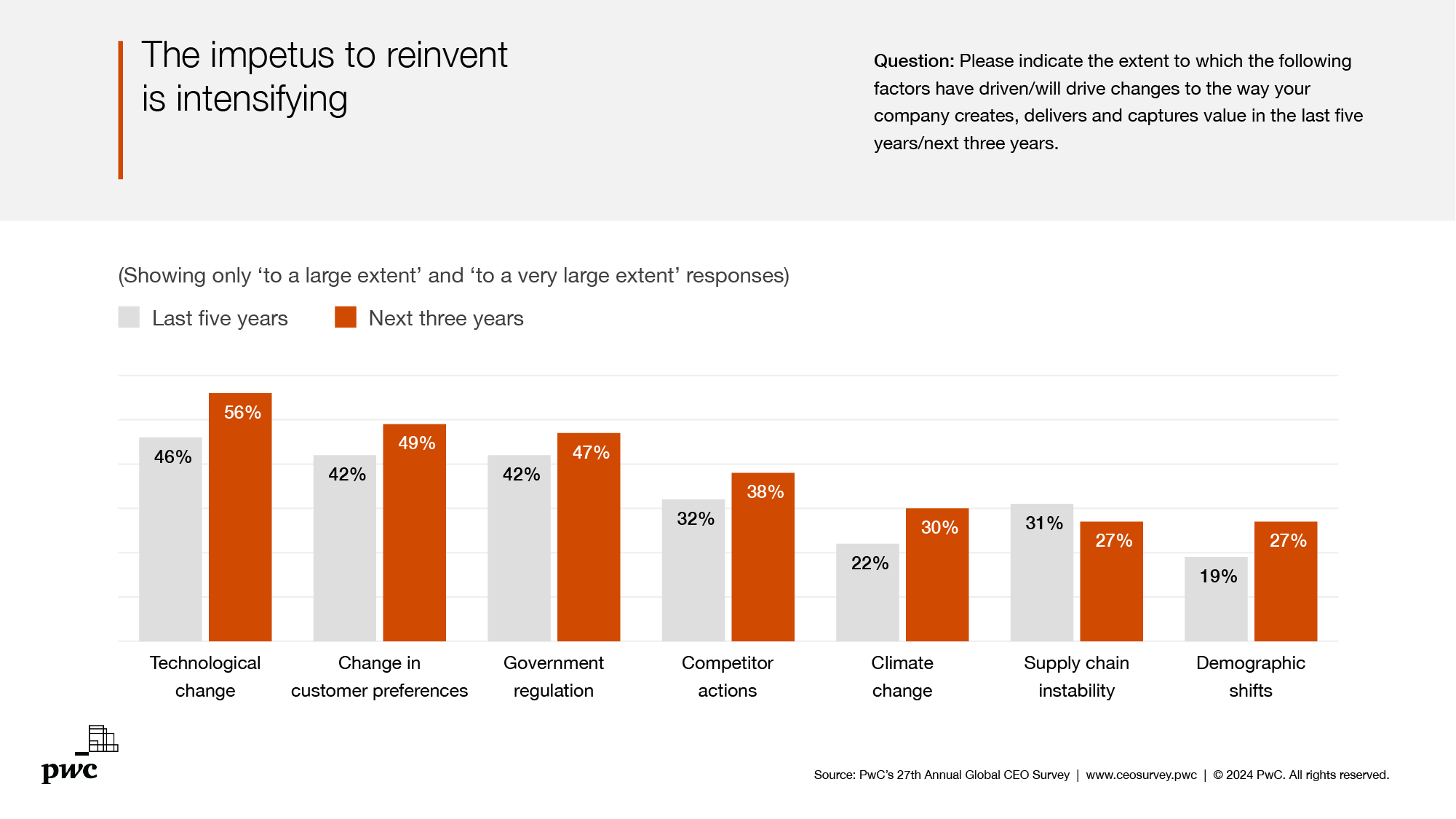

Another sign that the need to reinvent is rising is a notable increase in the pressure CEOs expect over the next three years from factors that influence business model change. Compared to the last five years, for example, CEOs expect changes associated with technology, customer preferences and climate change, among others, to have a far larger impact on the way they create, deliver and capture value. Only the impact of supply chain instability declines in relative terms as CEOs look ahead to the next three years.

{kind=link}

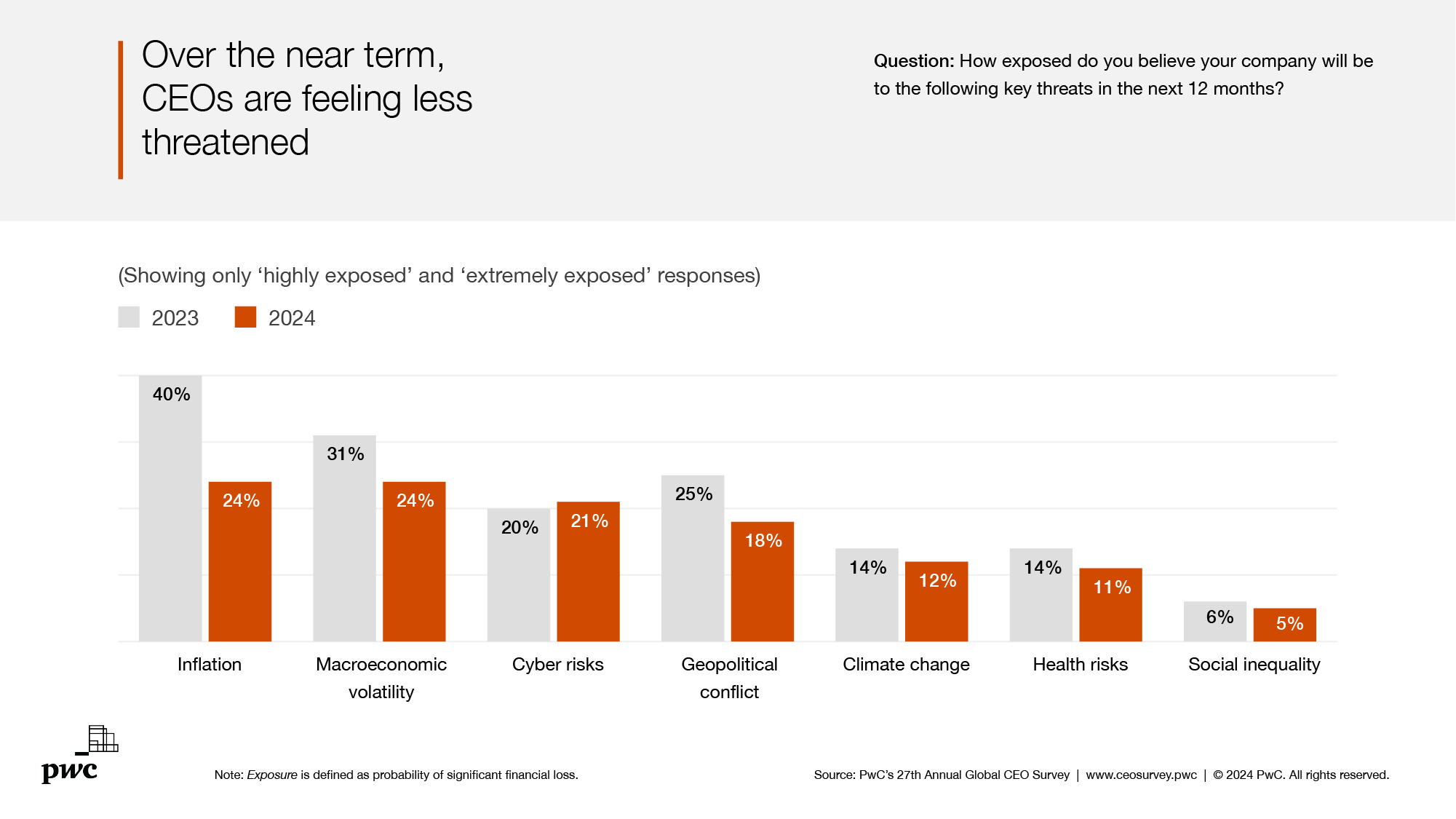

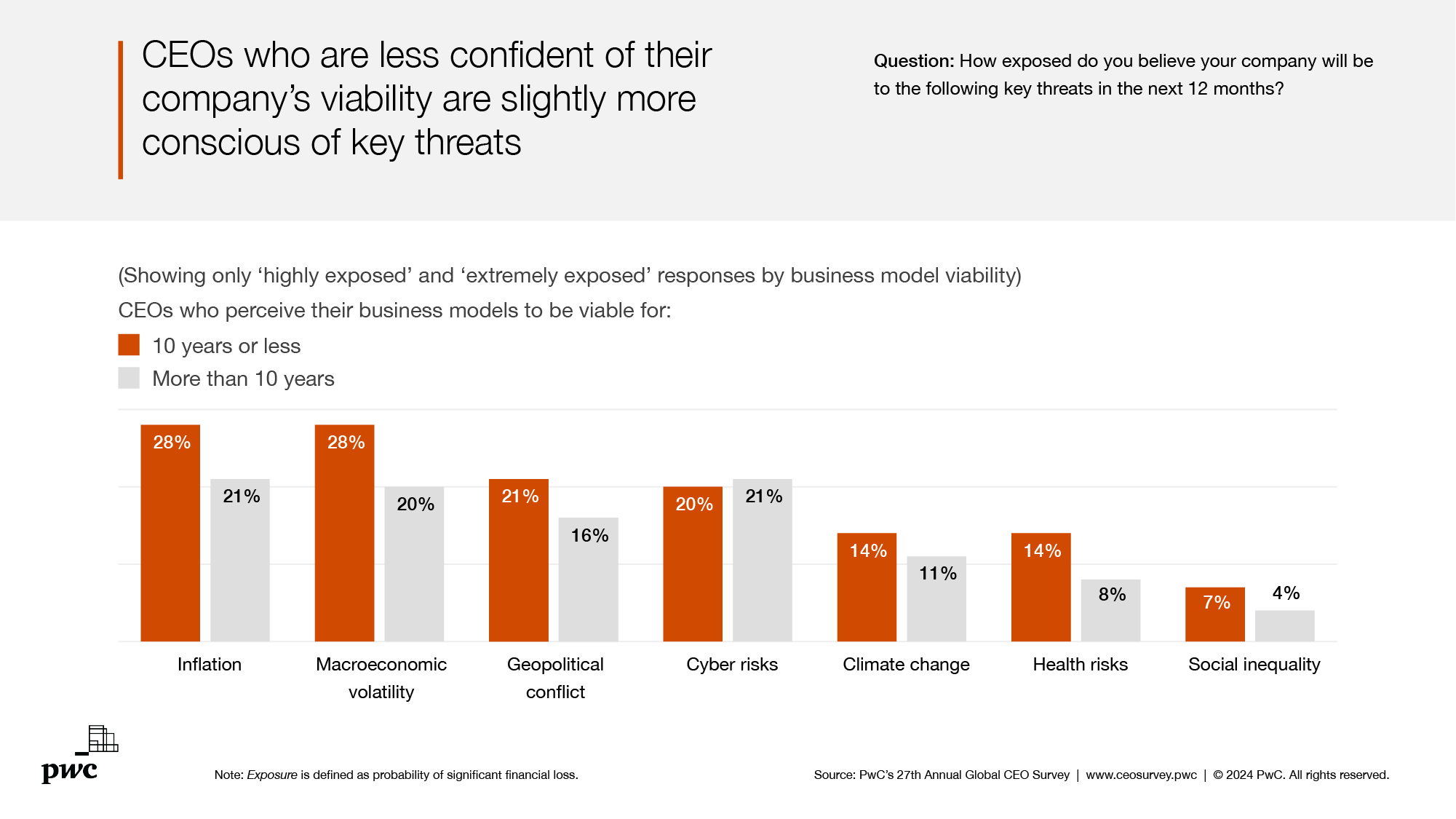

The growing importance of trends like these stands in contrast to CEO perceptions of exposure to several near-term threats, which have declined overall since last year. Geographically, however, CEOs still see pockets of concern. Inflation remains the top concern for CEOs in the United States, for example, despite receding in terms of expected exposure for global CEOs overall. Similarly, geopolitical threats are still among the top concerns for CEOs in Central and Eastern Europe, as well as the Middle East, despite receding for global CEOs overall. This may be because companies have already been taking measures to insulate themselves from the effects of some conflicts—and the full impact of others is still unclear. In Western Europe, CEOs are most concerned about cyber risk over the next 12 months—that’s especially true in France and Germany, where it’s perceived as the top threat. US CEOs also rank exposure to cyber risk high on their list of concerns.

{kind=link}

Looming existential change

3. Planetary work in progress

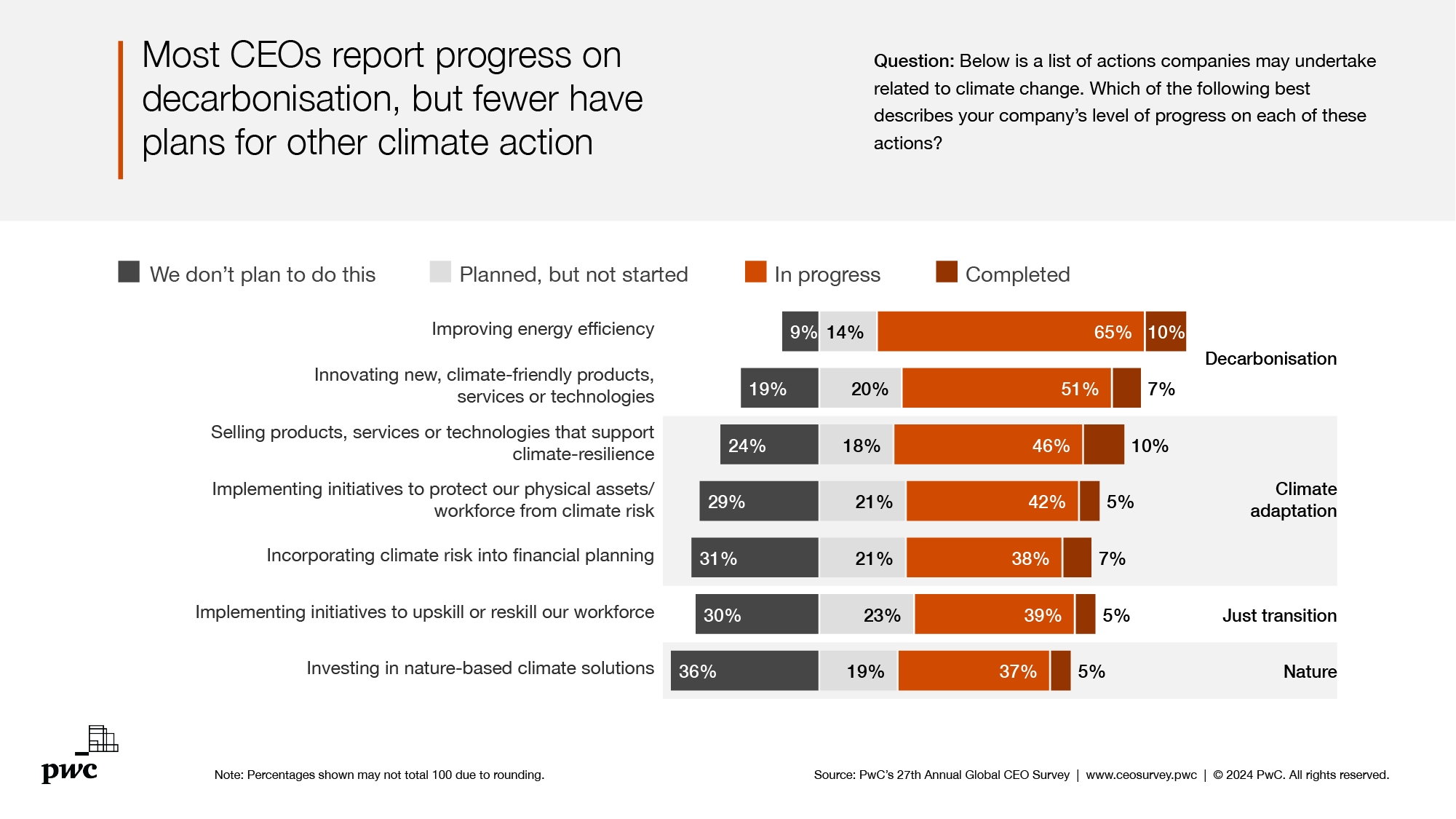

Among the megatrends pressuring CEOs to reinvent themselves, none is more important than climate change. Here, CEOs report mixed success at meeting their stated objectives. Roughly two-thirds have efforts underway to improve energy efficiency; another 10% report completing such initiatives; and about half say they have work in progress to innovate climate-friendly products or services. CEOs in Western Europe are more likely to have energy efficiency and climate-oriented innovation initiatives in progress or completed. And CEOs everywhere are accepting lower hurdle rates for climate-friendly investments, as we will explore later.

However, too many CEOs report having no plans for a range of other climate actions. For example, fewer than half of all respondents have incorporated climate risk into financial planning—and nearly one-third have no plans to do so. That may be because CEOs have:

- already factored climate risk into their insurance profiles with respect to recent severe weather events, without necessarily considering the long-term, chronic impacts of climate change

- only looked at what’s within their own corporate boundaries without fully considering the interdependencies in their supply chains.

55%

of global GDP—equivalent to about US$58 trillion—is moderately or highly dependent on nature, according to PwC estimates.

Among the other climate actions that CEOs say they aren’t likely to take are two with big societal implications. The first, upskilling or reskilling the workforce, is an important part of ensuring a just transition to a net-zero economy. The second, investing in nature-based climate solutions, will be vital if companies are to account for the surprisingly high dependence they have on nature. In fact, PwC estimates that 55% of global GDP—equivalent to about US$58 trillion—is moderately or highly dependent on nature.

{kind=link}

4. The AI opportunity

In addition to climate change, a second megatrend with systemic, existential implications is technological disruption. Specifically, our survey looked at generative AI, which has all the hallmarks of a technology that could significantly change how companies operate. It’s also approaching a critical juncture, seemingly poised to transform business models, redefine work processes and overhaul entire industries.

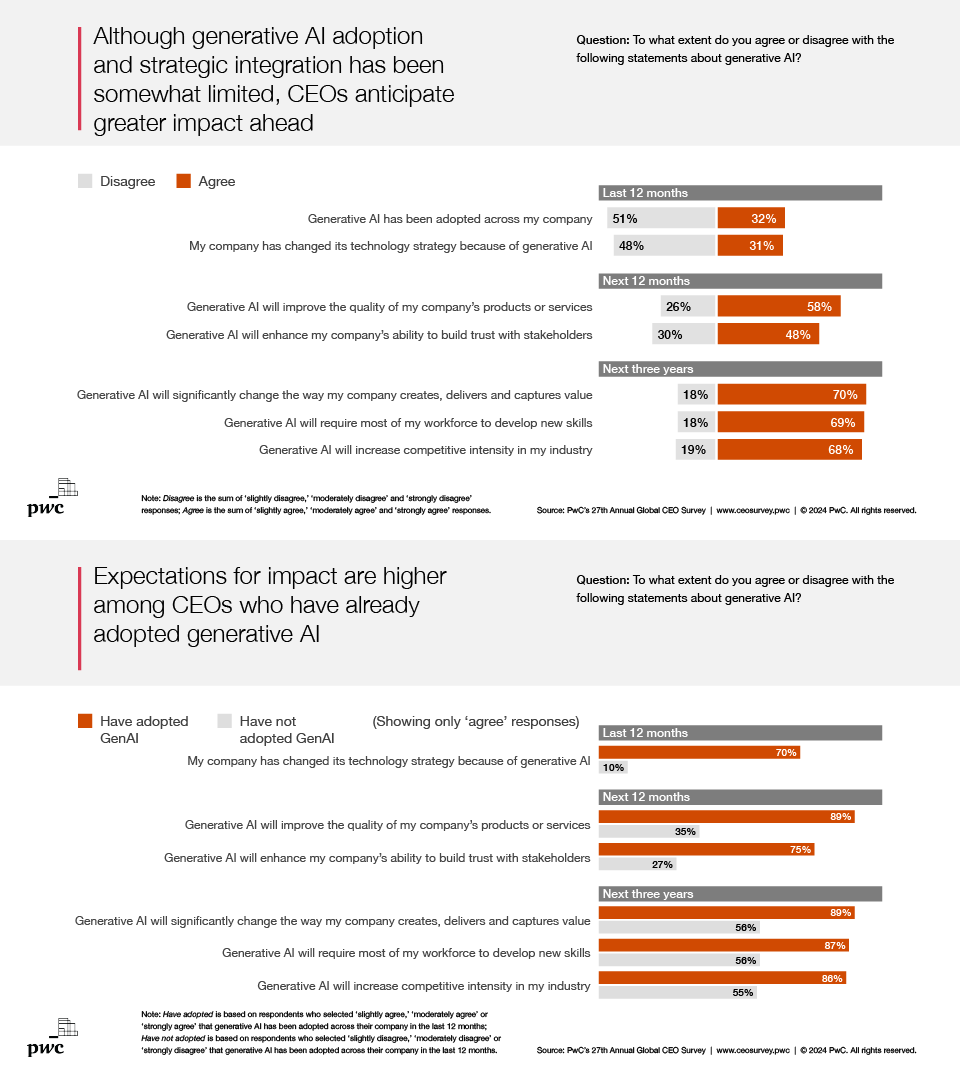

CEOs in this year’s survey appear to believe in both the fast pace of generative AI adoption and its outsized potential for disruption. For example, over the next year, about half of CEOs expect generative AI to enhance their ability to build trust with stakeholders, and about 60% expect it to improve product or service quality. Within the next three years, nearly seven in ten respondents also anticipate generative AI will increase competition, drive changes to their business models and require new skills from their workforce. So far, experience apparently buoys expectations. CEOs who say they have adopted generative AI across their company (about one-third of our sample) are significantly more likely than others to anticipate its transformative potential over the next 12 months, as well as over the next three years.

{kind=link}

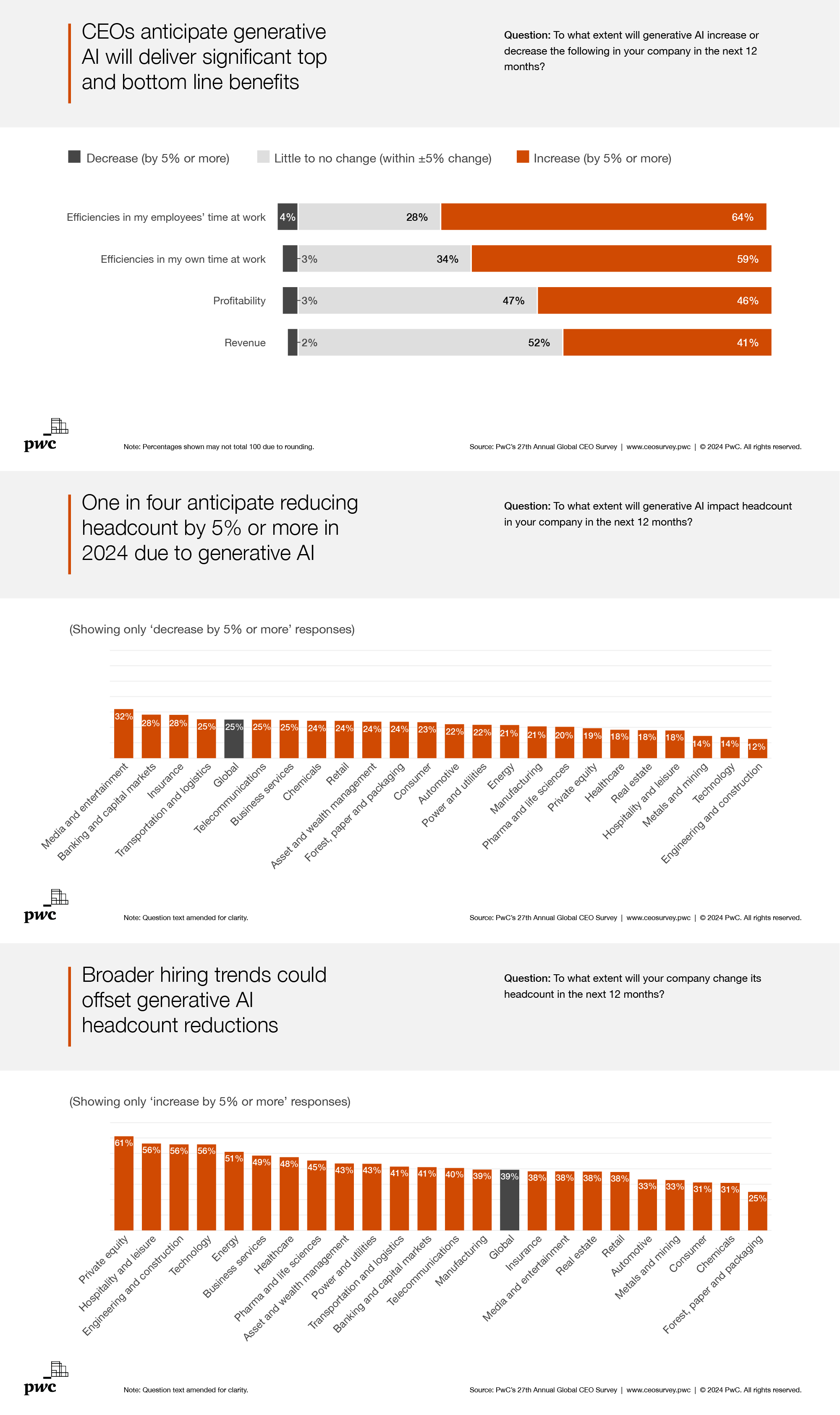

Overall, CEOs anticipate many positive near-term business impacts from generative AI. These include applications that increase revenues, such as through improved product quality and customer trust, as well as those that boost efficiency. This trend is consistent with PwC’s Global Risk Survey 2023, which found that 60% of respondents see generative AI as mostly or fully an opportunity rather than a risk.

At a societal level, the effects of generative AI are still uncertain. Some of those efficiency benefits appear likely to come via employee headcount reduction—at least in the short term—with one-quarter of CEOs expecting to reduce headcount by at least 5% in 2024 due to generative AI. Companies making early reductions to capture efficiencies in some areas may already be offsetting them with hiring in others, as growth and revenue opportunities become clearer. For example, although 14% of technology CEOs anticipate reducing headcount in the next year due to generative AI, 56% of them also anticipate hiring in 2024—at a rate almost 20 percentage points higher than the global average in our survey. (Overall, 39% of CEOs expect their company’s headcount to increase by 5% or more in the coming 12 months.)

These findings drive home the need for CEOs to bring their people along when it comes to generative AI. Being transparent, purpose-driven, and trusted regarding AI-related plans and decisions can help employees who are wary of AI (and what it may mean for their jobs) feel more comfortable experimenting—and innovating—with it. Ultimately, CEOs must embrace this as a new facet of their role: understanding, explaining and managing the inevitable tensions between short-term job losses and long-term job creation potential from AI.

{kind=link}

5. The AI challenge

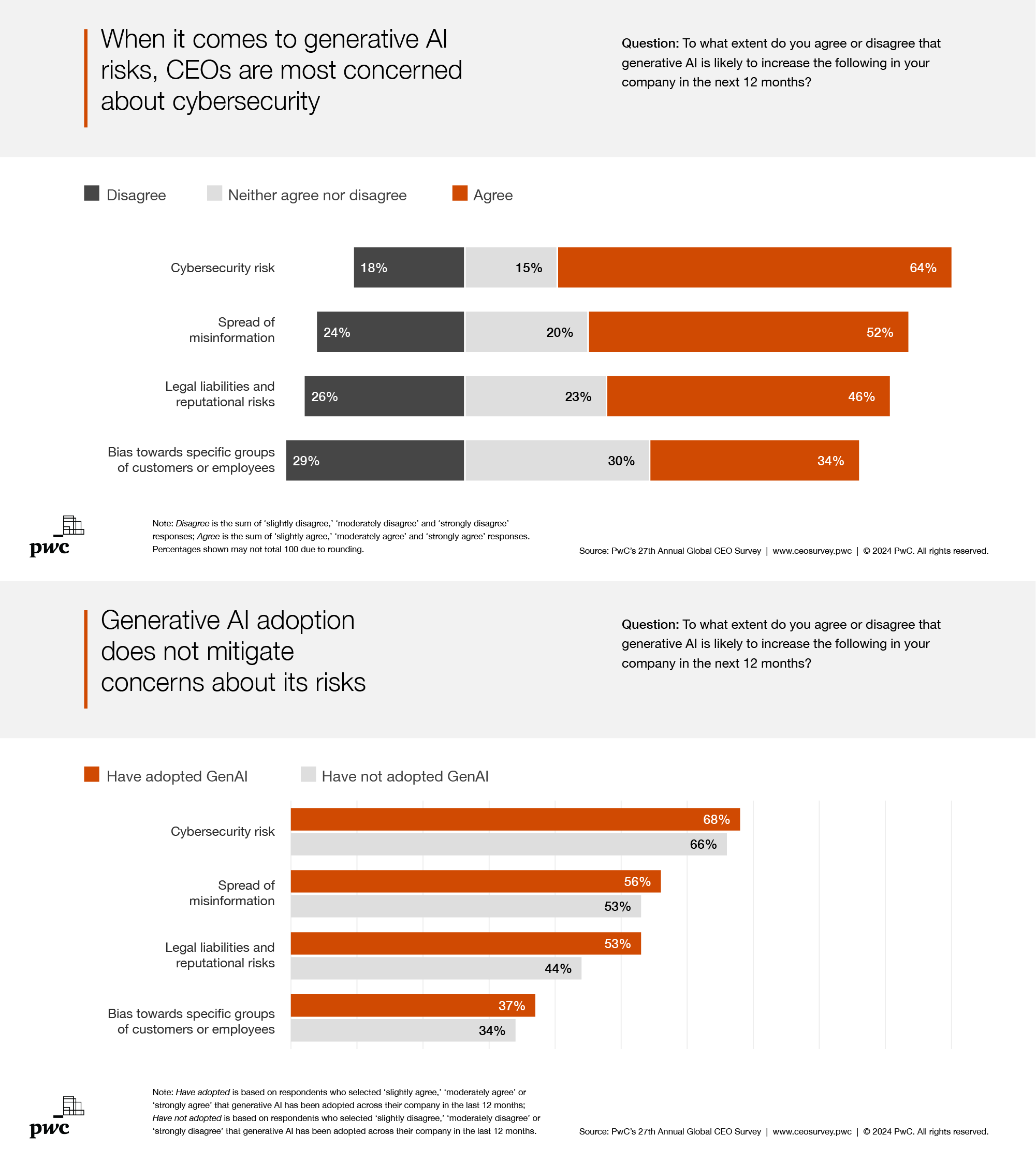

Even as the momentum of generative AI surges, a range of experts in the field are voicing concerns over the potentially significant, unintended consequences that could emerge as its reach grows. CEOs reflected similar sentiments in their responses to the survey. Consider, for example, that when it comes to generative AI, CEOs are most concerned about cybersecurity risk—and over half agree that it is likely to increase the spread of misinformation in their company. One-third of CEOs also expect generative AI to increase bias towards specific groups of employees or customers in the next 12 months. Almost as many disagree, suggesting bias is likely to be an area of growing attention as the scope and complexity of generative AI’s role in business expands. Interestingly, familiarity with generative AI does not seem to mitigate concerns about the risks among CEOs whose companies have already broadly adopted it.

{kind=link}

Taken together, these findings underscore the societal obligation that CEOs have for ensuring their organisations use AI responsibly. Indeed, given the pace of innovation and the inevitable delay in establishing new norms and regulations, much of the onus for managing this advancing technology falls, for now, to businesses. As Robert Playter, CEO of Boston Dynamics (a robotics manufacturer), told us in a recent interview, ‘While there are potential risks with [AI and large language models], we believe more in its potential and creating boundaries to mitigate any risk. This integration, like all applications of our robots, must adhere to…ethical principles, which strictly prohibit weaponizing the robots or using them for purposes of harm or intimidation.’

Your reinvention playbook

6. Turn barriers into opportunities

Armed with a better understanding of the challenges and the opportunities associated with meaningful business reimagination, CEOs can begin turning the former into the latter.

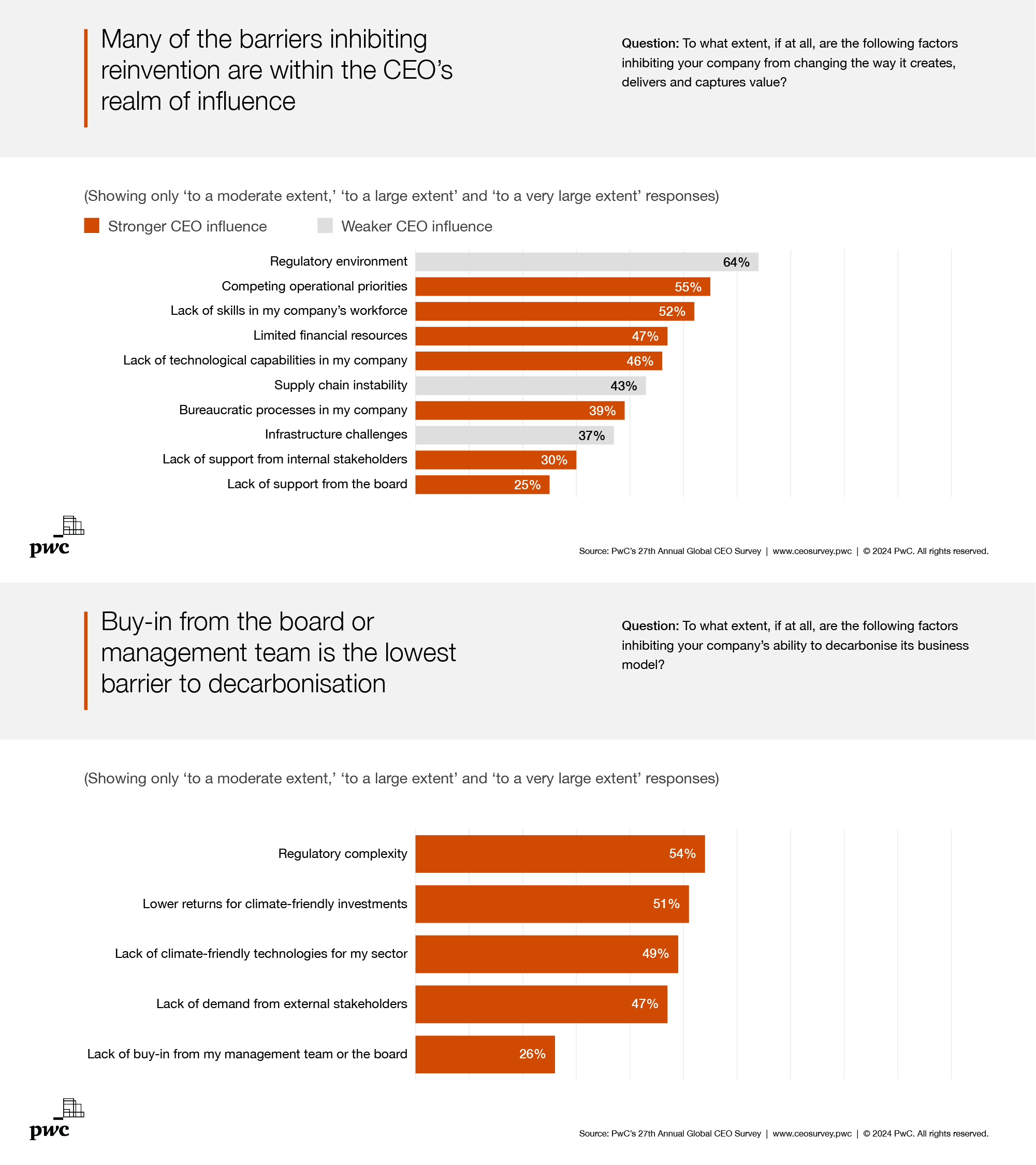

We asked CEOs about a range of obstacles they often confront when undertaking large-scale corporate change efforts. Their responses underscore that many constraints are sector-specific. Infrastructure challenges, for example, inhibit reinvention (to a moderate extent or more) in energy, power and utilities, and transportation and logistics (61%, 58% and 56%, respectively, compared to the global average of 37%). We also saw that CEOs who are more concerned about the viability of their companies were more likely to flag the existence of reinvention obstacles.

Additionally, though, we were surprised to learn how few CEOs perceived some obstacles to have much of an impact. For example, only 25% of CEOs described lack of support from the board as even a moderate constraint on their reinvention efforts, and only 30% of CEOs said the same of internal stakeholders. Similarly, only 26% of CEOs described a lack of support from the board or the management team as a moderate or greater constraint on decarbonising the company’s business model.

{kind=link}

On the other hand, many perceived constraints on reinvention fall squarely in a CEO’s realm of influence. Bureaucratic processes, competing operational priorities, limited financial resources, workforce skills and technological capabilities are subject to some degree of CEO influence—as is efficiency, which was an area of concern for many CEOs. On average, CEOs said that 40% of time spent on meetings, administrative processes and emails is inefficient. Moreover, respondents said that 35% of time spent in decision-making meetings, an activity over which CEOs often have direct personal control, is inefficient. Our conservative estimate of the cost of that inefficiency would be tantamount to a self-imposed US$10 trillion tax on productivity. That’s about 7% of global GDP at purchasing-power parity—what Harvard Law School professor Cass Sunstein might call a ‘sludge’ tax, borne of high transaction costs.

{kind=link}

7. Pinpoint your most important moves

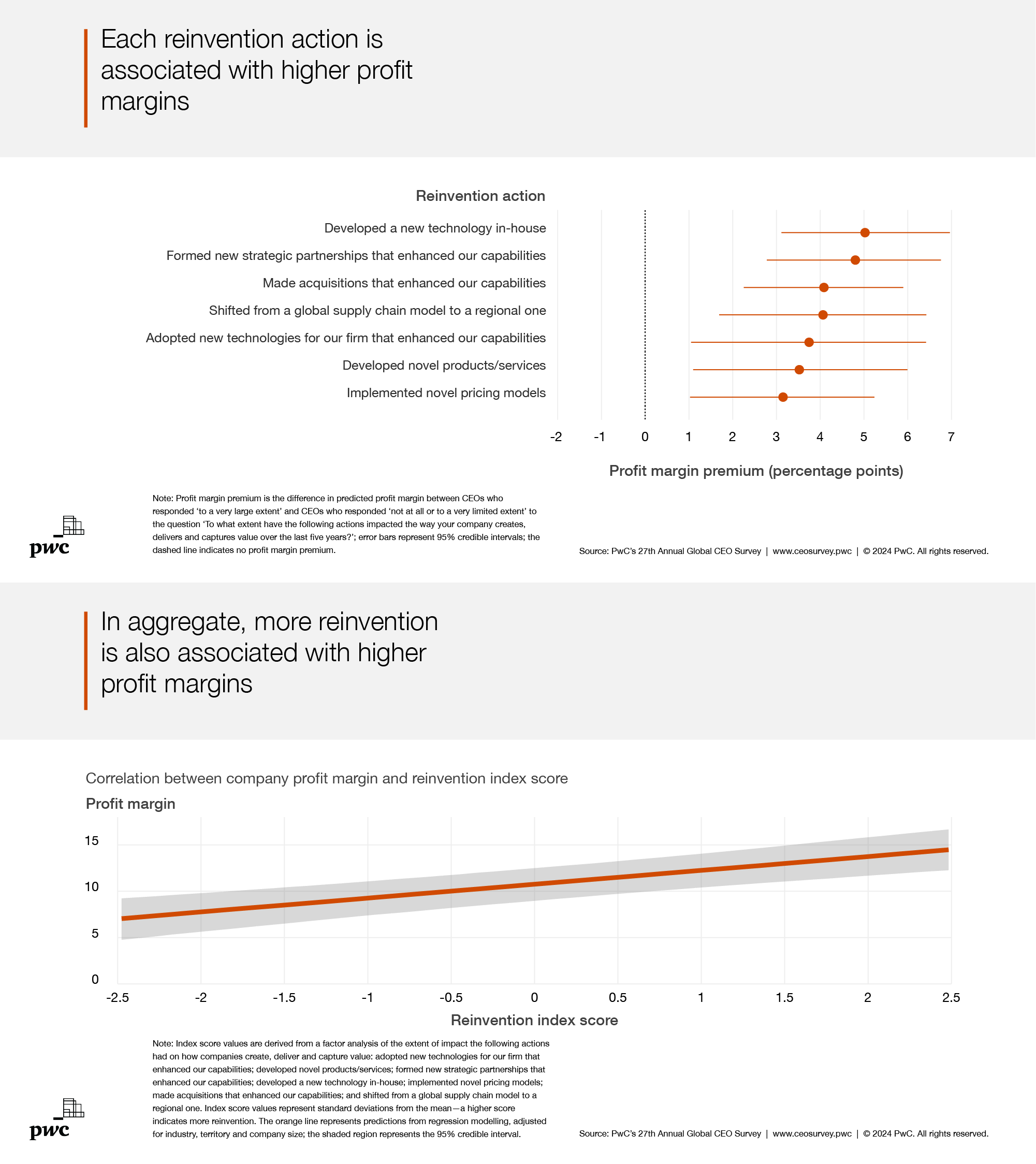

Actual progress will come when leaders and companies undertake meaningful initiatives to evolve the way they create, deliver and capture value. Analysis of this year’s survey data showed a positive association between self-reported profit margins and business moves that had a large or very large effect on respondents’ business models—such as technology development and deployment, novel pricing models, and strategic partnerships. This was true both of individual reinvention actions and of a composite reinvention index that we created. The data suggests that returns are three to five percentage points higher for actions with a very large impact on business models than those with limited impact.

{kind=link}

The right moves for each company will differ, of course, depending on its strategy, operating model, industry context and competitive landscape. Two things stand out. First is that nimble resource reallocation—an acknowledged attribute of high-performing companies—remains a critical area for CEO attention. Nearly two-thirds of CEOs reported reallocating 20% or less of resources from year to year, and almost 30% of CEOs cited resource reallocation of 10% or less. Higher levels of annual reallocation in the survey were associated with both greater levels of reinvention and higher profit margins.

28%

of CEOs report that their company reallocates 10% or less of its resources from year to year.

Second is the value of looking beyond a company’s walls and embracing business ecosystems. Separate PwC research finds it’s often possible to create more value than any firm could achieve alone by working across industry boundaries —through joint ventures or alliances, for example—to provide what customers need. Companies in ecosystems are 1.7 times as likely to be faster to market than peers, 1.2 times as likely to be flexible and agile, and 2.3 times as likely to be highly innovative.

{kind=link}

8. Recalibrate expectations for climate priorities

As CEOs establish priorities, many are seeing climate change as an industry disruptor containing distinct opportunities in addition to risks. Nearly one-third expect climate change to alter the way they create, deliver and capture value over the next three years—compared to less than one-quarter who said as much regarding the past five years. This may partly explain why 41% of CEOs, including over half of those at chemical companies, say their companies have set lower hurdle rates for climate-friendly investments than for other investments. Geographically, CEOs in Asia-Pacific are more likely than those elsewhere to have accepted lower hurdle rates, even though they were no more likely than CEOs elsewhere to report feeling highly or extremely exposed to climate change.

That’s consistent with the sentiment of investors in PwC’s Global Investor Survey 2023, two-thirds of whom say that companies should make expenditures that address environmental, social and governance (ESG) issues even if doing so reduces short-term profitability. Return requirements are critical inputs to corporate resource allocation decisions, so evidence that CEOs are flexing their expectations as they face up to the climate challenge is a hopeful sign of potential for progress. Related PwC research finds evidence, too, of a shift in private investor interest in green tech towards more emissions-intensive sectors.

{kind=link}

9. Keep your antennae up

‘Sooner or later,’ wrote the late Andy Grove, former CEO of Intel, in his 1996 memoir, Only the Paranoid Survive, ‘something fundamental in your business will change.’ Whether that change is in technology, intense competition or regulation, companies face forces that ‘build up so insidiously that you may have a hard time even putting a finger on what has changed, yet you know that something has.’

Facing inflection points that precipitate, in Grove’s words, ‘full-scale changes in the way business is conducted,’ managers must be ‘paranoid’ guardians of their businesses against competitors ‘who will eat away at it chunk by chunk until there is nothing left.’ Grove’s emphasis on sensing inflections made an appearance in a telling data point from this year’s survey. Those CEOs who are less confident in their company’s viability are more conscious of the threats they face. Whether that’s because they are at greater risk from those threats or because they’re seeing something other companies don’t probably varies by company, industry and geography. PwC’s Global Internal Audit Study 2023 highlights how effective a company’s risk, compliance and internal audit teams can be at putting in place the early-warning and risk-sensing systems to help spot these hazards.

{kind=link}

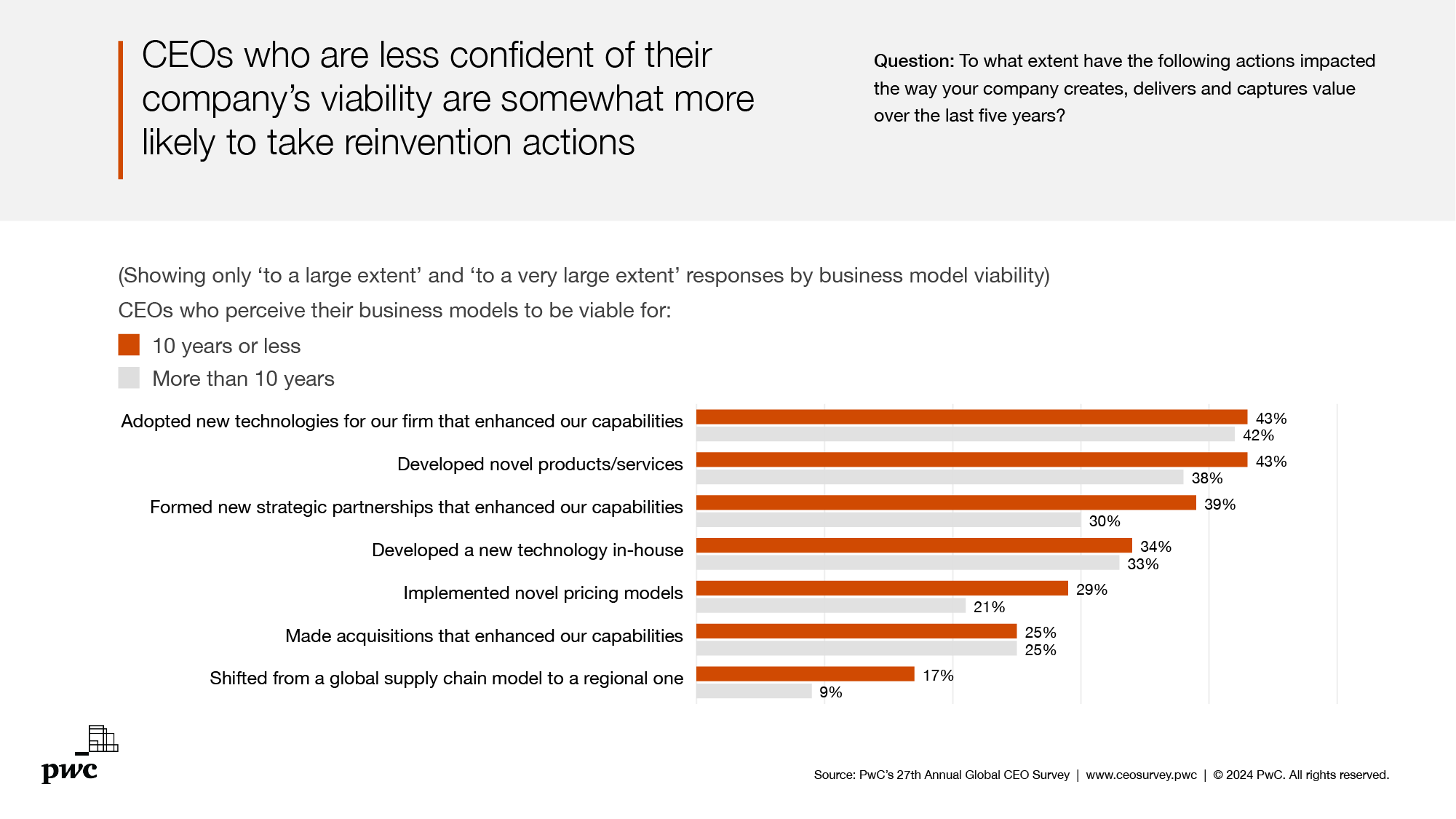

We also see CEOs who are more concerned about the viability of their businesses doing somewhat more to adapt than others. This was particularly true among CEOs who say their company formed new strategic partnerships, shifted from global supply chain models to regional ones, or implemented novel pricing models.

{kind=link}

Sustaining the change

The totality of this year’s survey results reflects an awareness among CEOs that they are navigating critical strategic inflection points, and feel a sense of urgency and a bias towards action. The data also suggest there’s a growing premium on leadership effectiveness to maintain energy, challenge the status quo and increase momentum. In a recent strategy+business article, PwC’s Ryan Hawk, Nadia Kubis and Blair Sheppard described a number of critical leadership priorities for reinvention-minded leaders.

For example, CEOs may need to expand their executive teams to include experts in emerging areas that are critical for their company’s future success, such as climate regulation or AI. Also crucial: having the whole top team own the change—as well as their systems of governance and control—rather than putting functional or business unit leaders in charge of discrete initiatives. In addition, many organisations will need to take account of the fact that the answers to a great many questions don’t exist, and new mechanisms will be necessary for solving problems together—rather than presenting solutions and seeking approval—as well as for new ways of tracking progress and rewarding people. What’s more, CEOs need a plan to communicate the urgency they are feeling, so that everyone understands and can potentially own part of the solution. People who are proficient at their current jobs may resist change because they’re concerned they may not be good at what they’ll be required to do in the future. So CEOs who are serious about reinvention must find approaches for acknowledging concerns, prizing curiosity and openness to learning, and encouraging managers to help people adapt.

Some of these leadership imperatives may sound familiar, but all of them raise expectations of CEOs to lead the voyage of strategic discovery necessary to evolve long-standing approaches to value creation. As we enter an age of continuous reinvention, CEOs have unparalleled opportunities to reshape their organisations, and themselves, to thrive on disruption, and transform aspirations into realities.

Get in touch

For questions about the data, including additional cuts, contact the CEO Survey research and analytics team.

For media inquiries, contact Dan Barabas.

Select a country or region from the list to explore local insights

Select country or region: Please select

Do you have an “early days” generative AI strategy?

Organizations at the forefront of generative AI adoption address six key priorities to set the stage for success.

The Leadership Agenda

Sharp, actionable insights curated to help global leaders build trust and deliver sustained outcomes. Explore our latest content on the global issues affecting organisations today from ESG to value creation, technology and cyber to workforce transformation.